Invisible Cavalry To The Rescue!

I’ve written a lot about the invisible bond vigilantes who have terrorized policy makers, even though there’s no actual evidence for their existence. But after Ben Bernanke’s speech this morning, it seems to be that I should also start writing about the invisible cavalry, which is always about to come to our rescue, but somehow never arrives.

Bernanke more or less admitted that the economic situation has developed not necessarily to America’s advantage, nothing like the growth he was predicting six months ago. But he argued that 2011 will be better, because … well, it was hard to see exactly why. He offered no major drivers of growth, just a general argument that businesses will invest more despite huge excess capacity, and consumers spend more despite still-huge debts and home prices that are likely to resume their decline.

Oh, and sure enough, he declared that inflation expectations are well-anchored, although the market says otherwise.

So: I guess this speech marked a small step toward QE2 and all that. But mainly the message was that just around the corner, there’s a rainbow in the sky.

So I’m going to have another cup of coffee, but skip the pie (in the sky).

Inflation And Interest Dynamics

Brad DeLong and Mark Thoma continue to suffer from dropped-jaw syndrome over the fact that (1) a Federal Reserve bank president believes that low interest rates lead to deflation (2) economists who think they’re being sophisticated are actually defending him.

I don’t really believe that a clearer explanation of what’s wrong with the Kocherlakota view will change anyone’s mind — my experience is that nobody ever admits that they were wrong about anything, and that this is especially true of economists who thought they were being sophisticated when they were actually failing Econ 101. But let’s give it a try, anyway.

So let’s look at it this way: instead of thinking of the Fed as setting the interest rate forever — which we’ve known since Wicksell it can’t do — think of it as following some kind of Taylor rule, in which the short-term interest rate depends positively on inflation and, maybe, negatively on the unemployment rate. This is feasible, as long as the coefficient on inflation is bigger than one.

Now suppose that it changes the rule, so as to set either a higher or a lower interest rate at any given level of inflation. What will happen to inflation and interest rates over time?

Suppose it shifts the Taylor rule up — that is, it tightens monetary policy, raising interest rates for any given set of economic conditions. This will, in fact, raise interest rates in the short run. However, over time inflation will fall, and in the long run lower inflation will be reflected in lower interest rates. This isn’t just theory: it’s what happened, with a few bumps along the way, in the great Volcker disinflation:

Conversely, a looser monetary policy will lead to lower rates in the short run, but higher rates in the long run.

What Kocherlakota and his defenders are doing is getting all of this backward: imagining that because in the long run low rates and low inflation go together, that loosening monetary policy — which reduces rates in the short run — actually causes disinflation and deflation. That is, as Brad says, cargo-cult economics; or to put it another way, it’s as if the Williamson family, noticing that families with high spending tend to have high net worth, assumed that it could raise its net worth by spending more.

Does this make things any clearer?

Slight edit for clarity.

Al, All Of The Time

For tomorrow’s column.

Ireland And Spain, Revisited

A couple of months back I asked, does fiscal austerity actually reassure markets? I noted there the curious case of Ireland, which embraced savage austerity early on; quite a few press reports declared that this had gained it the confidence of markets, but the actual numbers said otherwise. And I noted the contrast with Spain, which has been relatively slow and reluctant to embrace austerity, but has been treated no worse by investors.

Since then, the contrast has grown even more striking. Here’s the 10-year bond yield for Ireland:

And here’s the same for Spain:

Now, this isn’t a clean experiment: Ireland had an even bigger bubble than Spain did, so you could say that’s the issue. But since austerians were claiming bond market approval as a sign of its policy success, it is worth pointing out that dutiful Ireland looks as if it’s entering a runaway debt spiral, while malingering Spain is looking considerably better.

Anchors Away

Something I wanted to put up before the Jackson Hole extravaganza: let’s watch and see how many Fed officials declare that expectations of future inflation are “well-anchored” (which is the favorite formulation). Because, you know, they’re not.

Here’s a quick measure: the zero-coupon 5-year inflation swap, explained here. It looks like this:

Bloomberg

Bloomberg Some anchor.

Update: Yes, I know that the second word is spelled differently in the song. It’s deliberate on my part. No weigh would I get confused.

Hey, What About Trenton?

On behalf of the great state of New Jersey, I’m insulted: Trenton didn’t make this list of America’s 10 dying cities. OK, Atlantic City was on the list, but still.

We’re Still In A Paradox Of Thrift World

This morning Bloomberg has a story about how business investment — which was one of the few sources of strength lately — is flagging. Why? Because of concerns about overall economic growth.

This should serve as a reminder that we’re still very much in a paradox of thrift world.

In normal times, we believe that more saving, private or public, leads to more investment, because it frees up funds. But for that story to work, you have to have some channel through which higher savings increase the incentive to invest. And the way it works in practice, in good times, is that higher savings allow the Fed to cut interest rates, making capital cheaper, and hence on to investment.

But right now we’re up against the zero lower bound — yes, I’ll get the usual complaints about how long-term rates aren’t zero, but the Fed doesn’t have direct control over those rates — so this normal channel doesn’t work.

And what that means is that if people — or the government — try to save more, they only end up depressing the economy. And the weaker economy leads to lower, not higher investment. And this in turn means that attempts to save more don’t help our future prospects. On the contrary, they reduce the economy’s future growth.

That’s why fiscal austerity is such a terrible idea: no only does it raise unemployment, it actually makes us poorer in the long run.

Nick Rowe Loses It

And good for him.

He has a piece about the Kocherlakota claim that a policy of keeping interest rates low will lead to deflation, and is shocked to find “new monetarist” Stephen Williamson agreeing. The fun stuff is in the comments (all items from Rowe):

W (as quoted by Marcus):

“In this case, I agree with Kocherlakota, that the market has it wrong. As Kocherlakota argued, most of our monetary models tell us that, if the Fed maintains a constant nominal interest rate target forever, that will essentially determine the inflation rate, by way of the Fisher relation.”

Oh Christ. Oh Christ. Oh Christ.

SW interprets Kocherlakota the same way I do, and thinks he’s right. Oh Christ.

…

Oh Christ.

Central banks can’t keep the price level and inflation rate determinate by pegging the nominal (or even real) rate of interest forever. We’ve known that was wrong at least since Wicksell’s cumulative process. I assumed that everyone (except a few hopeless lefties and funny money guys) knew that was wrong. *Nobody’s* monetary model tells us that (except a few hopeless Post Keynesian types, who are at least logically consistent, because they assume very sticky prices that don’t respond to AD at all).

Oh Christ.

…

This is much worse than Cochrane getting Say’s Law wrong. Say’s Law is very nearly right, and very few people understand precisely why say’s Law is wrong, and that it’s money, and only money, and not any other asset, that makes Say’s Law wrong.

I give up.

This isn’t New Monetarism. It’s got nothing to do with Monetarism at all. It’s the exact opposite of Monetarism. Somebody resurrect Milton Friedman.

Yup.

Fire Alan Simpson

I always thought that the deficit commission was a bad idea; it has only looked worse over time, as the buzz is that Democrats are caving in to Republicans, leaning ever further toward an all-cuts, no taxes solution, including a sharp rise in the retirement age.

I’ve also had my eye on Alan Simpson, the supposedly grown-up Republican co-chair, who has been talking nonsense about Social Security from the get-go.

At this point, though, Obama is on the spot: he has to fire Simpson, or turn the whole thing into a combination of farce and tragedy — the farce being the nature of the co-chair, the tragedy being that Democrats are so afraid of Republicans that nothing, absolutely nothing, will get them sanctioned.

When you have a commission dedicated to the common good, and the co-chair dismisses Social Security as a “milk cow with 310 million tits,” you either have to get rid of him or admit that you’re completely, um, cowed by the right wing, that IOKIYAR rules completely.

And no, an apology won’t suffice. Simpson was completely in character here; it was perfectly consistent with everything else he’s said, and with his previous behavior. He has to go.

Krugman or Paulson: Who You Gonna Bet On?

Sorry, can’t resist. That was the title of this Business Week article a few months ago. The tone made it pretty clear that if you had any sense, you’d ignore the bearded academic and go with the market wizard:

If [Krugman] makes you want to head for the hills with your shotgun and turnip seeds, consider another view, expressed the week prior at the London School of Economics. The speaker was not a decorated academic with visions of 1873, he was a profit seeker, pure and simple: John Paulson, the hedge-fund manager on whose behalf Goldman Sachs (GS) cooked up those killer collateralized debt obligations designed to pay off handsomely in the event of a housing crash. He was right about that one, you’ll recall.

“We’re in the middle of a sustained recovery in the U.S.,” Paulson declared in London. “The risk of a double dip is less than 10 percent.” The housing market is now, he says, an attractive buying opportunity. “It’s the best time to buy a house in America,” he said. “California has been a leading indicator of the housing market, and it turned positive seven months ago. I think we’re about to turn a corner.”

No mention of a third depression.

So, how’s it going? I’m sure that if Paulson had proved right, there would be a followup article mocking yours truly. Wanna bet that there won’t be a piece saying that maybe professors know something that traders don’t?

There Are Bubbles, And Then There Are Bubbles

On the whole, I find it amazing and distressing that fear of new bubbles is playing such a large role in current policy discussion, leading too many prominent economists to recommend raising interest rates in the face of a hugely depressed economy. Even if you believe that excessively low policy rates were a key reason for the housing bubble — which I don’t — the idea that we should be raising rates now brings to mind the old joke about the motorist who runs over a pedestrian, then tries to fix the damage by backing up, and running over the pedestrian a second time.

Beyond that, I think we need to bear in mind that while bubbles are in general a bad thing, just how bad depends a lot on the context — in particular, whether the inflation of the bubble has been accompanied by a big increase in leverage on the part of those buying the inflated assets.

Consider the stock bubble of the late 1990s. It was crazy, and when it popped U.S. households suffered a capital loss of about $5 trillion. This was bad, and helped cause a recession. But it never rose to the level of economic catastrophe.

Then came the housing bubble, after which households suffered a capital loss of about $8 billion trillion [hey, a few zeroes more or less ... ]. Yes, they also suffered a big loss as stocks plunged — but that was because the housing bust, unlike the stock bust, had a huge impact on the financial system and the economy as a whole.

What was the difference? First, a lot of financial institutions — which are highly leveraged — were holding securities whose value was highly sensitive to the state of the housing market. There was nothing comparable in the case of stocks. So the housing bust undermined the financial system in a way the stock bust never did.

Second, households also leveraged themselves up in the housing boom, in a way they for the most part didn’t with stocks (yes, there were people buying dotcoms on margin, but they were not typical). So the housing bust created a balance-sheet crisis for the household sector in a way that the dotcom bust didn’t.

The moral for right now is that even if you believe that there are bubbles inflating or about to inflate, they’re only a big concern if they are leading to leveraged positions for key players. The alleged carry trade bubble sorta kinda mighta have met that criterion, although I never found the warnings all that persuasive. But other stuff — bubbles in BRIC equities, or gold, or whatever, don’t make the grade.

Anyway, my point is not so much about current events as a more general observation: the bubbles we should fear are those that lead to leverage, and set us up for a Minsky moment.

The WSJ Changes Its Line

This morning, in its “Vital Signs” feature (not online, for some reason), the WSJ notes the plunge in interest rates, and says:

In April, when the economy looked healthier and it was believed the Federal Reserve would raise rates by year end, the 10-year yield approached 4%.

But that’s not what the same newspaper said — in its news section, not its editorial page — back when rates actually were near 4%. Instead, it ran an article titled Debt Fears Send Rates Up; Unease At Deficit Hurts Demand For Treasurys.

There’s a reason I keep harping on this. It’s not the fact that lots of people made a bad forecast; that’s going to happen now and then. it’s the fact that people were pushing a theory — a theory that said that we had to be terribly afraid of those bond vigilantes — which had no basis in actual evidence. Yet you wouldn’t have known that from reading the financial news media, which reported this theory, not as a hypothesis, but as fact.

There was no evidence whatsoever, back in April, that debt fears were driving rates up. But the WSJ reported this completely made-up view as truth, without even a hint that it had weak (or, actually, zero) empirical support. In effect, news reporting became propaganda on behalf of a political agenda.

I’m glad to see the WSJ now giving a more accurate account — but it’s a bit late, and the fear of invisible bond vigilantes has already done immense damage.

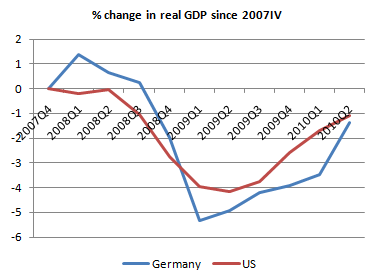

What About Germany?

Many people are now holding Germany up as proof that austerity is good.

There are a number of reasons that’s foolish, among them the fact that Germany’s austerity policies have not yet begun — up to this point they’ve actually been quite Keynesian.

But it’s also worth having some perspective on actual German performance to date. Here’s a chart:

Eurostat

Eurostat Everything you’ve been hearing is about that uptick at the end. But I’m not willing to declare an economy that has yet to recover to the pre-crisis level of GDP an economic miracle.

Basically, here’s the German story: it’s an economy that didn’t have a housing bubble, so it wasn’t caught up directly in the bust. But it’s very export-oriented, with a focus on durable manufactured goods. Demand for these goods plunged in the early stages of the crisis — so that Germany, remarkably, had a bigger GDP decline than the bubble economies — but has bounced back since summer 2009. This has pulled Germany back up; exports to China have done especially well.

If there’s a slam-dunk argument for austerity in there, it’s remarkably well hidden.

Orwell And Social Security

I have to say, after Bush’s Social Security scheme collapsed five years ago, I never thought I’d be back over the same old ground so soon.

But Social Security is actually a key testing ground — it’s the place where you really see what people are after, and also get a sense of whether they’re at all honest about what they’re trying to do.

So: Pat Toomey supports replacing much of Social Security with a system of private accounts, but denies that this is privatization — and denounces those who use the term:

Iâve never said I favor privatizing Social Security. Itâs a very misleading â itâs an intentionally misleading term. And it is used by those who try to use it as a pejorative to scare people

Oh, my. Back in the 1990s the Cato Institute had something called The Project on Social Security Privatization, which issued papers like this one from Martin Feldstein: Privatizing Social Security: The $10 Trillion Opportunity.

Then the right discovered that “privatization” polled badly. And suddenly, the term was a liberal plot — hey, we never said we’d do that.

Wait, it gets worse: Cato not only renamed its project, but it went back through the web site, trying to purge references to privatization. Bush also tried to deny that he had ever used the word. More here.

And here we go again. So remember who originally called privatization privatization: the privatizers, that’s who.