On my way to Berlin and beyond. Posting will be erratic.

China Raises Rates

As if to illustrate my point about the non-equivalence of the United States and China: China raises interest rates.

So, the United States is pursuing an expansionary domestic monetary policy, which increases overall world demand; however, a side consequence of this policy is a weaker dollar. China is pursuing a weak-yuan policy; to counter the inflationary domestic effects of that policy, it’s pursuing a contractionary domestic monetary policy, reducing overall world demand.

We’re doing the right thing; they’re making the world as a whole worse off.

Just Call Him Bernanke-sama

Mark Thoma points us to a paper by Mary Daly of the San Francisco Fed, which contains this remarkable chart of core inflation in two episodes:

From Seven Samurai to The Magnificent Seven, this time in economics.

Even More On The Origins of the Deficit

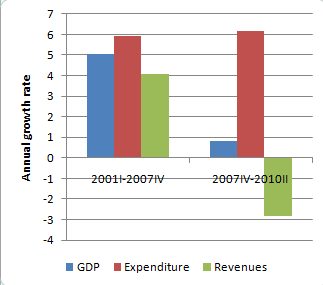

I’ve thought of another way to present the data on GDP, spending by all levels of government, and taxes. Let’s look at trends in GDP, spending, and revenues over two periods — one designed to capture “normal” growth, the other the economic crisis.

For the first period, I look at trends from the business cycle peak in the first quarter of 2001 to the peak in the last quarter of 2007. This is a standard way of measuring economic trends, by the way, since business cycle peaks presumably measure the economy’s output at or near capacity. And yes, this means that I wrote this post in a fit of peaks.

For the second period, I use the quarters since that 2007 peak.

So here’s what you get:

Bureau of Economic Analysis

Bureau of Economic Analysis During the pre-crisis period, spending grew slightly faster than GDP — that’s Medicare plus the Bush wars — while revenue grew more slowly, presumably reflecting tax cuts.

What happened after the crisis? Spending continued to grow at roughly the same rate — a bulge in safety net programs, offset by budget-slashing at the state and local level. GDP stalled — which is why the ratio of spending to GDP rose. And revenue plunged, leading to big deficits.

But I’m sure that the usual suspects will find ways to keep believing that it’s all about runaway spending.

We’re Not China

In various comments and other places I keep seeing people compare European complaints about the weak dollar to American complaints about the undervalued renminbi. It’s a false equivalence, which should be obvious if you think about the basics of the situation.

What the United States is doing is an expansionary monetary policy in the face of a depressed economy and threats of deflation; what else do you expect us to do? Now, one effect of that policy, if it isn’t matched abroad, is a weaker dollar — but that’s not the goal of the policy.

Beyond that, the overall effect of quantitative easing in America is expansionary for the world economy as a whole: expansionary in the United States, and ambiguous for the rest of the world. (It’s ambiguous because there are two effects: the weaker dollar tends to reduce the US trade deficit, but a stronger US economy tends to increase the deficit, with the net effect uncertain.)

Now compare this with China’s situation. China isn’t fighting deflation — it’s fighting inflation, so the undervaluation of the yuan has to be accompanied by restrictive credit policies domestically. (China can separate exchange rate policy from domestic monetary policy because it has capital controls). The overall effect of the policy is therefore to reduce, not increase, world demand — and the effect on foreign economies is clearly negative.

The policies, then, aren’t at all equivalent.

What about the argument that America can offset any effects from China’s policies through looser money? Well, I don’t really get why some commentators can’t grasp the distinction between the proposition “quantitative easing is worth trying, and would probably help” and the proposition “quantitative easing will allow the Fed to do whatever is needed, never mind the zero lower bound.” I subscribe to the first, not the second. And since QE is likely to be helpful but inadequate, China’s artificial surplus adds to the shortfall.

So again, the Fed is moving in the right direction, both for US interests and for the sake of the world as a whole. China is beggaring its neighbors, which in this case means everyone else.

The Unbearable Slowness of Understanding

OK, I’m about to be unfair. But this article about how the Fed is gradually coming to realize that low inflation and a liquidity trap might be a problem fills me with despair.

I mean, we’ve been there for two years:

It was obvious to me, soon after Lehman fell, that this was the big one — that we were well on our way to a lost decade unless decisive action was taken quickly. Yet we’ve spent most of the last two years worried about the wrong things — inflation, crowding out, invisible bond vigilantes.

Even now, we get things like this:

Many economists remain confident that the United States will avoid the stagnation of Japan, largely because of the greater responsiveness of the American political system and Americans’ greater tolerance for capitalism’s creative destruction. Japanese leaders at first denied the severity of their nation’s problems and then spent heavily on job-creating public works projects that only postponed painful but necessary structural changes, economists say.

There are multiple things wrong with that paragraph — but what on earth would give one reason to consider our political system “responsive”? The truth is that we’re responding worse than Japan did.

And yes, I’m depressed about it.

Epitaph For An Administration

In today’s report on the foreclosure mess, a revealing sentence:

As the foreclosure abuses have come to light, the Obama administration has resisted calls for a more forceful response, worried that added pressure might spook the banks and hobble the broader economy.

Surely this can serve as a generic statement:

As NAME ISSUE HERE has come to light, the Obama administration has resisted calls for a more forceful response, worried that added pressure might spook the banks and hobble the broader economy.

Stimulus, bank rescue, China, foreclosure; it applies all along. At each point there were arguments for not acting; but the cumulative effect has been drift, and a looming catastrophe in the midterms.

Or to put it another way, the administration has never missed an opportunity to miss an opportunity. And soon there won’t be any more opportunities to miss.

Why Have Deficits Exploded?

For all those commenters saying that we must have had a surge in government spending — I mean, look at the deficit! — a simple picture:

Government spending has continued to rise more or less on its pre-crisis trend. Revenue has plunged, because the economy is deeply depressed.

Other questions?

Core Logic, Again

Every once in a while it seems necessary to explain why, when considering monetary policy, we need to focus on inflation measures that exclude volatile prices like food and energy. So, read this.

The Non-Surge In Government Spending, Continued

A bit more on how government spending has not, contrary to what you hear everywhere, surged under Obama. Let me offer a calculation that will, I hope, make things a bit clearer. (Cue the usual suspects shouting that I’m lying).

So, what would we have expected total government spending — federal, state, and local — to do over the past three years if there had not been a crisis and a change in government control? A first approximation would have been spending growing along with the trend growth in the economy — that is, real GDP growing with the economy’s potential, and government spending growing at real GDP plus inflation.

Now, over the period 2000-2007 — from business cycle peak to business cycle peak — real GDP grew 2.4 percent a year. So a reasonable estimate for trend growth is 2.4 percent, or 7.3 percent since 2007.

We can use actual inflation: the GDP deflator rose 4.1 percent from 2007II to 2010II.

Put these together, and “normal” growth in government spending would have been 11.7 percent over the past three years.

Actual growth has been higher: 19.5 percent. So government spending is about 7 percent, or about $350 billion, higher than a simple trend projection would have suggested. What accounts for the higher spending?

Well, none of it is government consumption; it’s all in transfer payments. BEA data aren’t quite as helpful here as I’d like, but it’s clear that a large chunk, roughly $100 billion, is unemployment benefits, which have surged along with unemployment, and another large chunk is Medicaid spending, which has surged because the slump has impoverished more people. Some more for other safety net programs, like food stamps. Also, Social Security and Medicare outlays have gone up about $85 billion more than my 11.7 percent norm — medical cost growth, aging baby boomers, and maybe some people taking early retirement because they can’t find jobs.

And with that, you’ve basically explained the growth in government spending. No giant expansion of the welfare state — just business as usual in the face of a horrific slump.

A Fine European Whine

Here:

A senior European policy-maker, who asked not to be named, said a further aggressive round of monetary easing by the US Federal Reserve would be “irresponsible” as it made US exports more competitive at the expense of its rivals.

In other words, how dare you act to protect your economy from deflation and double-digit unemployment? By doing so, you make our inappropriate tight-money policy even more destructive!

The Boehnerization of Barack Obama

Why has stimulus become a dirty word? Many reasons, I guess: an inadequate plan combined with a wildly overoptimistic forecast was more or less guaranteed to create the impression of a failed program. But it’s also true that the president himself has had a deeply self-destructive tendency to echo his opponents’ arguments. My original invisible bond vigilantes post was inspired, in part, by Obama’s decision to go on Fox News and declare that we needed to cut the deficit to avoid a double dip. Then, in July, he repeated almost verbatim John Boehner’s justly mocked claim that since the private sector is tightening its belt, the government should do the same.

And he’s done it again:

Nonetheless, Obama said that just as people and companies have had to be cautious about spending, “government should have to tighten its belt as well. We need to do it in an intelligent way. We need to make sure we do things smarter, rather than just lopping something off arbitrarily without having thought it through.”

As I wrote back in July,

We’ll never know how differently the politics would have played if Obama, instead of systematically echoing and giving credibility to all the arguments of the people who want to destroy him, had actually stood up for a different economic philosophy. But we do know how his actual strategy has worked, and it hasn’t been a success.

The Nipponization of Ben Bernanke

I’m with Brad DeLong on Bernanke’s speech: given Bernanke’s diagnosis of our problems, what he said about the policy response was astonishingly diffident:

… the FOMC is prepared to provide additional accommodation if needed to support the economic recovery and to return inflation over time to levels consistent with our mandate. Of course, in considering possible further actions, the FOMC will take account of the potential costs and risks of nonconventional policies …

True, it’s a stronger statement than we’ve seen in the past. But with unemployment near 10 percent and headed up, core inflation below 1 percent by most measures and headed down, the Fed is edging toward modest action, while worrying about the risks?

What I have always suspected is that the real risk the Fed fears is that it will do unconventional stuff but fail to move the economy, and hence lose face — which was the primary reason the Bank of Japan was so unwilling to act back when Professor Bernanke used to criticize it. So it’s important to understand two things: first, this should not be a consideration — the Fed’s job is to save the economy, not its own reputation. Second, half-hearted measures are a good way of guaranteeing that unconventional policy fails.

The only thing I guess you can say is that the Bernanke Fed is better than, say, the ECB. But that’s not saying much.

Big Spender Update

Menzie Chinn takes on the same territory I’ve examined here and here. The key picture:

That uptick in transfers at the end is mainly unemployment insurance, plus some Medicaid — that is, it’s safety-net spending in the face of high unemployment.

It’s kind of interesting to read Menzie’s comments — many of which assert that he must have left something out. You see, they know that there has been a huge expansion of the government, and any facts suggesting otherwise must be wrong.

Meet The Elite

Max Abelson in the New York Observer:

“The first thing that needs to happen, I think, is to get these people out of their homes,” a man wearing a bespoke blue-striped shirt, a Hermés tie patterned with elephants and Ferragamo loafers said recently. “Correct! I’ll explain,” the veteran member of a bank restructuring and advisory team said.

Read the whole thing.